Charles Spinelli Debunks the Business Insurance Strategies for Expanding Companies

Facing new opportunities and increased risks go hand in hand as businesses grow. Business progression is all about introducing new...

Charles Spinelli Debunks the Business Insurance Strategies for Expanding Companies

Charles Spinelli Debunks the Business Insurance Strategies for Expanding Companies

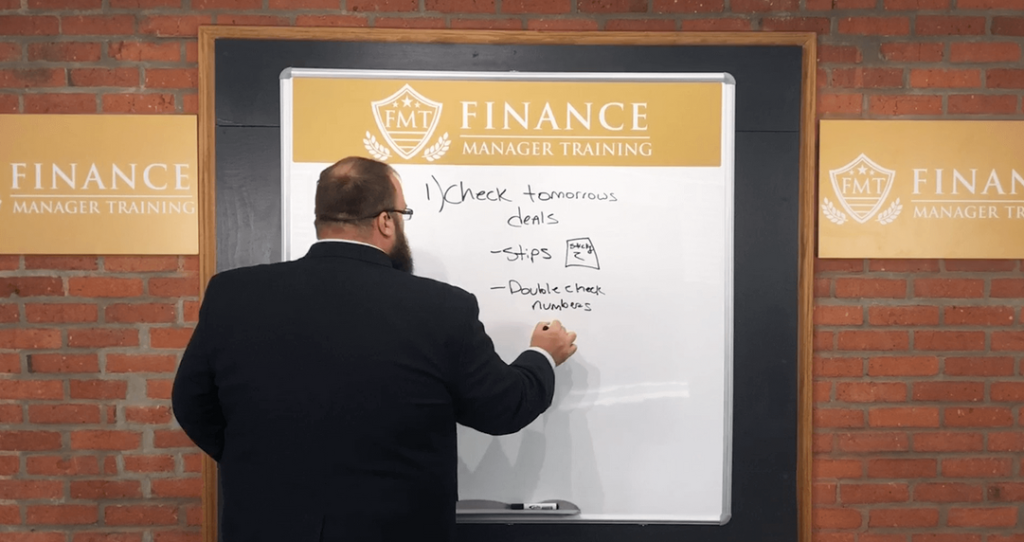

Why Online F&I Training Is A Smart Move For Car Dealership Owners

Why Online F&I Training Is A Smart Move For Car Dealership Owners

Undergraduate Student Loans: What I Wish I’d Known Before Borrowing

Undergraduate Student Loans: What I Wish I’d Known Before Borrowing

Why Zero-Cost EMI on Electronics Is Not Always Interest-Free

Why Zero-Cost EMI on Electronics Is Not Always Interest-Free

Inside the Process: How High-Purity Hydrocarbon Streams Are Produced

Inside the Process: How High-Purity Hydrocarbon Streams Are Produced

Facing new opportunities and increased risks go hand in hand as businesses grow. Business progression is all about introducing new...

Running a car dealership is not simple anymore. Customers do more research before they walk in. Lenders expect cleaner paperwork....

Interest rates on student loans can pile up, resulting in hefty debt thanks to capitalization, where unpaid interest adds to...

Shopping for a new smartphone or a high-end laptop often leads us to the same tempting offer. You see a...

Pure hydrocarbons run the chemical industry. Without them, no plastics. No solvents. No synthetic materials. However, crude oil is extracted...

The collections landscape has transformed completely. Ten years ago, auto lenders ran their operations with phone banks and filing cabinets....

For property owners in Utah, understanding the costs of asphalt paving is essential for budgeting residential or commercial projects. Prices...

A missing bolt can stop a billion-dollar assembly line. One factory fire in Thailand might delay aircraft deliveries for months....

Dubai has become one of the most attractive destinations for entrepreneurs and investors worldwide. With a strong economy, business-friendly regulations,...

The digital revolution has fundamentally changed how we interact with financial institutions. Not long ago, the process of borrowing money...